Convertible and renewable term life insurance can make a basic term policy more flexible. A standard term life insurance policy gives coverage for a fixed period. Your health may change, your mortgage may last longer than expected, your children may still depend on your income, or you may later want lifetime protection.

Convertible term life insurance and renewable term life insurance matter. One gives you the option to convert temporary coverage into permanent life insurance. The other may let you renew coverage after the original term ends. Both features can help avoid coverage gaps.

Recent industry research shows that many families still feel underinsured. LIMRA and Life Happens reported that 42 percent of American adults said they need life insurance or need more of it. That makes it important to understand policy features before buying.

Convertible and Renewable Term Life Insurance: Quick Overview

Convertible and renewable term life insurance are policy features that may be included in some term life insurance contracts.

| Feature | Convertible Term Life Insurance | Renewable Term Life Insurance |

| Main Purpose | Convert to permanent life insurance | Renew term coverage |

| Medical Exam | Usually not required for conversion | Usually not required for renewal |

| Premium Change | Usually increases after conversion | Usually increases at renewal |

| Coverage After Action | Permanent coverage | Continued term coverage |

| Best For | Future lifetime coverage needs | Short term coverage extension |

A convertible term life insurance policy helps if you want affordable coverage now but may want permanent coverage later. A renewable term life insurance policy helps if you may need to extend term coverage without starting a new application.

What Is Convertible Term Life Insurance?

Convertible term life insurance is a term policy that allows the policyholder to convert some or all of the term coverage into a permanent life insurance policy. This is called term life insurance conversion.

So, what is convertible term life insurance in simple words? It is temporary coverage with a built in option to switch to permanent coverage later, usually without proving your health again.

For example, a parent may buy a 20 year term policy because it is affordable. Ten years later, their health changes. If the policy has a conversion option, they may be able to convert part of the coverage into whole life insurance or universal life insurance.

Convertible term life insurance may help people who want:

- Lower premiums at the beginning

- Future lifetime coverage

- Protection if health changes

- Estate planning flexibility later

- A bridge between temporary and permanent life insurance

If you want affordable coverage now with flexibility for the future, you can explore term life insurance coverage options that match your family, mortgage, and income protection needs.

How Term Life Insurance Conversion Works

Term life insurance conversion allows you to change a term policy into a permanent policy during a specific conversion period. The insurance company may let you convert to whole life insurance, universal life insurance, or another permanent life insurance product.

The key benefit is that converting term life insurance usually does not require a new medical exam. Your new premium will still be higher because permanent life insurance costs more than term coverage, but your health may not be reviewed like a brand new application.

| Conversion Factor | What It Means |

| Conversion Period | Time window when conversion is allowed |

| Conversion Option | Right to change term coverage to permanent coverage |

| New Premium | Usually based on age and permanent policy type |

| Medical Exam | Often not required |

| Available Policies | Depends on the insurance company |

The phrase term conversion life insurance usually refers to this process. It is not a separate policy type. It means using your conversion privilege to move from temporary coverage to permanent life insurance.

Benefits of Convertible Term Life Insurance

Convertible term life insurance gives flexibility. It is especially useful when your current budget supports term coverage, but your future goals may require permanent life insurance.

Main benefits include:

- You can start with affordable term coverage.

- You may convert without a new medical exam.

- You can protect your insurability if health changes.

- You may get lifetime coverage later.

- You can support long term financial or estate planning goals.

A convertible term life insurance policy can be helpful for young families, business owners, new homeowners, and people with growing income. It lets you protect your family today while keeping future options open.

Limitations of Convertible Term Life Insurance

Convertible term life insurance is useful, but it is not unlimited. Every policy has rules. Some policies allow conversion only during the first several years. Others allow conversion until a certain age or before the term ends.

Common limitations include conversion deadlines, higher premiums after conversion, limited permanent policy choices, partial conversion rules, and an option that can expire if you wait too long. Before buying, ask when the conversion period ends, what permanent policies are available, and whether you can convert only part of the coverage.

What Is Renewable Term Life Insurance?

Renewable term life insurance allows the policyholder to continue coverage after the original term ends, usually without a new medical exam. In simple terms, a renewable term life insurance policy can be renewed if the contract allows it and premiums are paid.

This can help if you still need life insurance but do not want to apply for a new policy. For example, your 20 year term policy may end while you still have a mortgage, dependent spouse, or business debt. Renewing term life insurance may help you keep coverage for a while longer.

Renewable term life insurance is often used for short term extended protection, coverage gaps, mortgage or debt continuation, temporary income replacement, changed health conditions, and families not ready to lose protection.

How Renewing Term Life Insurance Works

Renewing term life insurance means continuing the policy after the original term expires. The insurance company may allow renewal for a set number of years or up to a certain age.

However, renewal does not mean the price stays the same. Renewal premiums usually increase because they are based on your current age. The older you are, the higher the risk to the insurer, so the cost usually rises.

| Renewal Factor | What It Means |

| Renewal Option | Ability to continue coverage |

| New Medical Exam | Usually not required |

| Premium | Usually increases at renewal |

| Renewal Limit | May end at a certain age |

| Coverage Type | Remains term life insurance |

A renewable term life insurance policy can be renewed, but it may become expensive over time. That is why renewal is often better for short term needs rather than long term planning.

What Is Annual Renewable Term Life Insurance?

Annual renewable term life insurance is a policy that renews one year at a time. It provides coverage for one year, and the policyholder can usually renew each year for a certain period without new proof of insurability.

| Feature | Annual Renewable Term Life Insurance |

| Coverage Length | One year at a time |

| Renewal | Usually yearly |

| Medical Exam | Usually not required at renewal |

| Premium | Usually increases each year |

| Best For | Short term or temporary needs |

Annual renewable term life insurance may work for someone who needs coverage briefly, such as while waiting for employer benefits, closing a business loan, or finishing a temporary obligation. It may not be ideal for someone who wants predictable long term premiums.

Benefits of Renewable Term Life Insurance

Renewable term life insurance gives policyholders a way to extend protection without starting over.

Benefits may include:

- Continued coverage after the term ends

- Usually no new medical exam

- Helpful if your health has changed

- Useful for temporary extended protection

- Can cover short term debt or family needs

- May prevent a life insurance coverage gap

Renewable term life insurance can be practical when your need for protection lasts longer than expected. It can give your family more time while you decide whether to buy a new policy, convert coverage, or reduce your insurance needs.

Limitations of Renewable Term Life Insurance

The biggest limitation is cost. Renewing term life insurance often becomes expensive because premiums rise with age. A policy that was affordable during the original term may become costly after renewal.

Other limitations include limited renewal periods, sharp premium increases, no lifetime guarantee, no cash value, and rules that depend on the original contract. Renewable term life insurance is useful, but it should not be treated as a permanent solution unless the cost and terms make sense.

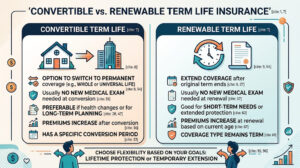

Convertible vs Renewable Term Life Insurance

Convertible and renewable term life insurance both add flexibility, but they solve different problems.

| Comparison Point | Convertible Term Life | Renewable Term Life |

| Main Action | Convert the policy | Renew the policy |

| Result | Permanent life insurance | Continued term insurance |

| Purpose | Lifetime coverage option | Temporary extension |

| Medical Exam | Often not required | Often not required |

| Premium Change | Higher permanent premiums | Higher age based premiums |

| Best Use | Long term planning | Short term protection gap |

Choose convertible term life insurance if you may want lifetime coverage later. Choose renewable term life insurance if you only need to extend term coverage for a limited time.

Cost Factors to Consider

The cost of convertible and renewable term life insurance depends on several factors.

| Cost Factor | How It Affects the Policy |

| Age | Older age usually increases premiums |

| Health | Affects original policy pricing |

| Coverage Amount | Higher death benefit costs more |

| Term Length | Longer terms may cost more upfront |

| Renewal Timing | Later renewal usually costs more |

| Conversion Timing | Later conversion may increase permanent premiums |

| Policy Type | Permanent coverage usually costs more than term |

The important point is that conversion and renewal both protect flexibility, but neither guarantees the same low premium forever.

Common Mistakes to Avoid

Many policyholders buy term life insurance and forget to review it. That can lead to missed deadlines or expensive decisions later.

Avoid these mistakes:

- Waiting too long to convert your policy

- Assuming renewal premiums will stay level

- Ignoring the conversion deadline

- Not asking which permanent policies are available

- Relying only on employer life insurance

- Forgetting to update beneficiaries

- Letting the policy lapse by missing payments

- Not comparing new coverage options

A yearly policy review can help you avoid surprises.

Who Should Consider These Policy Features?

Convertible and renewable term life insurance may help people whose financial needs can change, including young parents, homeowners, business owners, people with dependents, spouses needing income protection, and anyone planning for estate needs later.

Convertible coverage may be better if you want long term flexibility. Renewable coverage may be better if you only need a temporary extension.

Questions to Ask Before Buying

Before choosing a policy, ask clear questions.

- Can this term policy be converted?

- What is the conversion deadline?

- Which permanent policies are available?

- Can the policy be renewed after the term ends?

- How much will renewal cost?

- Are renewal premiums guaranteed?

- Is a medical exam required?

- Can I convert part of the coverage?

- Are riders available?

- What happens if I miss a payment?

These questions help you understand the policy before your family depends on it.

Final Thoughts

Convertible and renewable term life insurance can both make term coverage more useful. Convertible term life insurance helps if you may want permanent life insurance later. Renewable term life insurance helps if you may need to extend coverage after the original term ends.

The right option depends on your budget, health, dependents, mortgage, income, business obligations, and long term financial goals. If you want flexibility, read the policy terms closely and ask about conversion and renewal rules before you buy.

A good term life insurance policy should not only protect your family today. It should also give you smart options for tomorrow.

FAQs

What is convertible term life insurance?

Convertible term life insurance is a term policy that allows you to convert some or all coverage into permanent life insurance during a specific conversion period.

What is renewable term life insurance?

Renewable term life insurance allows the policyholder to renew coverage after the original term ends, usually without a new medical exam.

Can a renewable term life insurance policy be renewed?

Yes, a renewable term life insurance policy can be renewed if the contract allows it and premiums are paid. Premiums usually increase at renewal.

What is annual renewable term life insurance?

Annual renewable term life insurance provides coverage for one year at a time and can usually be renewed yearly for a set period.

How does term life insurance conversion work?

Term life insurance conversion lets you change a term policy into a permanent life insurance policy, often without a new medical exam.

Is converting term life insurance a good idea?

Converting term life insurance may be a good idea if you want lifetime coverage, your health has changed, or you need permanent life insurance for long term planning.

Does renewing term life insurance increase premiums?

Yes, renewal premiums usually increase because they are based on your age at renewal.

Which is better, convertible or renewable term life insurance?

Convertible term life insurance is better for future permanent coverage. Renewable term life insurance is better for short term extended protection.